Observations from the Latest Quarterly Reports – Sysco, US Foods & PFG

We are pleased to provide our most recent foodservice industry update containing our observations and thoughts on the latest quarterly earnings releases from the three largest publicly traded foodservice distributors. Our comments were developed from each company’s quarterly announcement, the transcripts from investor calls and our independent research.

The main themes reported in this round of calls are similar to those we heard during the prior quarter:

- Overall, a favorable environment for product demand.

- Generally moderate food cost inflation.

- Continued operating expense pressure, primarily from wages.

- Development of technology tools to attract and retain customers.

- Moderating / Declining diesel fuel prices.

While we expand on each of these five themes in various sections of this edition of our Foodservice Industry Update, we felt it might be helpful to summarize how independent distributors might benefit from some of the public companies’ initiatives.

Takeaways for Independent Foodservice Distributors

Here are several areas where virtually all independents could explore the initiatives underway at the larger companies. In some instances, it may be valuable to seek outside assistance to help design and implement some of the following changes.

Personnel

— Develop and improve recruitment, onboarding and training of drivers and warehouse workers.

— Review all pay programs to determine if wages are competitive.

Operations

— Review truck routing for efficiency and customer satisfaction.

— Review fleet composition – should trucks for non CDL drivers be added?

Customer Profitability

— Review pricing to determine if gross profit dollars can be increased without sacrificing volume.

— Analyze customer mix, vendor mix, and item mix to assure the best return.

— Evaluate sales rep incentive programs to assure they are driving growth in profitability.

Information and Technology

— Assure all business intelligence tools are being used fully to drive profitable growth.

— Revisit financial and operational reporting to ensure management has the tools necessary to manage both the day to day decisions as well as develop more strategic initiatives.

The Five Main Themes From This Quarter’s Reports

The main themes reported in this round of calls are similar to those we heard during the prior quarter:

1. Foodservice Distributor Market Commentary

Overall case growth for the three largest public distributors during the quarterly period ending September 29, 2018 vs. the same prior year period are as follows:

| Sysco | U. S. Broadline Local Case Growth (Organic) | 3.7% |

| US Foods | Independent Case Growth (Organic) | 3.1% |

| PFG | Independent Case Growth – Foodservice | 4.8% |

Note: Each of these companies defines independent/local cases differently.

Some of the commentary provided on the calls appeared to present slightly different views.

George Holm, President & CEO of PFG stated “We still have the stated goal of running 6% – 10% case growth…. but I will state that we have got to have a healthy industry to do that.”

Sysco added the “restaurant industry saw improved performance, particularly in same-store sales growth despite lower same-store traffic”.

US Foods reported they believe the outlook for independent restaurants was strong and that the restaurant count was up year over year. They predicted volume growth of 4% in the “independent restaurant” sector for the year.

US Foods also commented they have seen no growth in their existing health care customer portfolio. This could indicate weakness in the sector or the continued impact of GPO’s.

2. Tight Labor Market Remains a Challenge

All of the foodservice distributors indicated that the labor markets remain tight. Warehouse employees and drivers are particularly in demand. Drivers are hard to recruit away from other employers, and according to some distributors, do not want the same levels of overtime as they may have in the past – forcing many companies to find additional drivers. Warehouse workers also have a number of options for employment, including online retailers like Amazon.

While PFG, US Foods and Sysco are employing similar strategies to deal with these tight labor markets, each company is not necessarily employing all of the examples shown here.

Increasing Wages – For certain types of employees and in certain geographies, they have raised entry level wages in order to attract talent. For instance, US Foods said it was raising entry wages in selected markets.

Improving Recruiting and Training – Improving the recruiting process as well as enhancing entry level training was highlighted by both US Foods and Sysco in their commentary. PFG believes improved training can help reduce turnover and increase employee retention, particularly in the first year of employment.

More Effective Routing – Each distributor indicated they continuously work on routing to take miles out of the system while also maintaining (or improving) customer service. This can help mitigate the need for additional drivers and also help fuel expense (less miles = less fuel).

Utilizing Different Vehicles – It continues to be hard to recruit CDL A drivers. Some of the “big three” have increased their use of vehicles that do not require a driver with a CDL A designation. We are seeing this approach from some of the independents as well.

Pricing – Where possible, each distributor reported trying to thoughtfully pass on price increases to offset some of the rising operational costs.

3. Technology as a Differentiator

All three companies continue to invest in technology offerings to make their customers more efficient and effective.

- PFG announced a small investment in a technology company called Omnivore.

- US Foods, in the recent earnings call, said “we continue to grow our penetration of sales going through our industry-leading e-commerce platform. And we continue to see greater adoption of our value-added solutions on the part of our customers”.

- Sysco is advertising “MySysco” which provides instant access to Sysco digital tools and applications from a single touchpoint. MySysco advises that it will provide its customers with a one-stop shop for ordering, bill payments, tracking, and more.

Technology solutions also remain a key focus for many of the independent distributors we speak with. They comment that keeping up with changing customer demands is a critical factor in remaining relevant in the marketplace. Time will tell how customers view these tech enhancements.

4. Food Cost Inflation Remains Mild

Based on the commentary from these earnings calls, we feel overall food cost inflation remains mild. Here is some of the commentary we heard on the calls:

- “Deflation has been a little more prevalent in several commodity categories…” Dirk Locascio, CFO & Principal Accounting Officer, US Foods

- “Overall, food cost inflation for the quarter was approximately 0.6%. We witnessed deflation sequentially from the fourth quarter through the first quarter. Deflating items include meat, poultry and cheese. We also witnessed some items inflating such as eggs, disposables and frozen foods.” James Hope, Executive VP & CFO, Performance Food Group

- “….it’s a slowing down of the inflation that we had planned but [we] are also seeing deflation in a couple of key categories….” Thomas Bene, President, CEO & Director, Sysco

- “…in our FreshPoint business, for example, we had fairly significant deflation in the produce area….” Joel Grade, Executive VP & CFO, Sysco

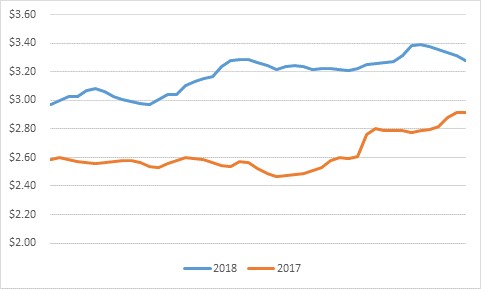

5. Diesel Fuel Prices

Diesel fuel prices for the week of November 19, 2018 averaged $3.28 nationally, still nearly 13% over the comparable price from the same week a year ago. While prices remain elevated relative to last year, we have seen prices come down from peak levels in October 2018. Additionally, the year to year price gap has narrowed.

With the price of crude falling in the global market, we believe there is reasonable optimism for fuel prices to continue to slide, barring supply disruption in the market.

Weekly Price of U.S. Diesel Fuel ($/Gallon) Through Week of 11/19/2018

Market Conditions and Consumer Sentiment

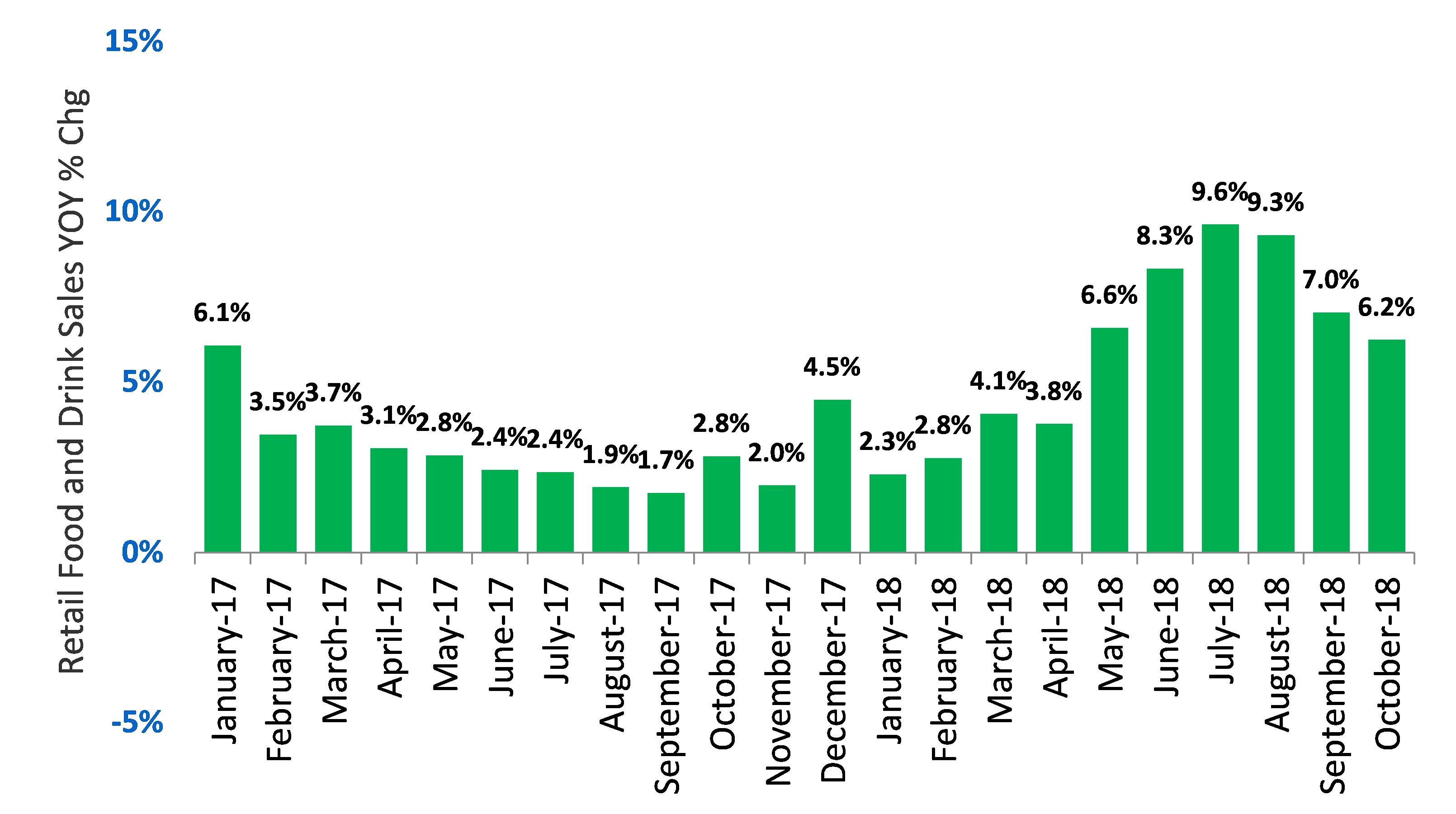

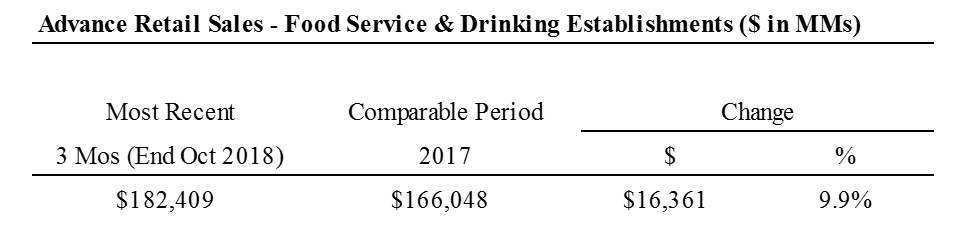

Overall, macroeconomic conditions in the U.S. remained favorable. U. S. food and drink retail sales continued to show strong growth, with year-over-year increases remaining above 5%. It is likely the increases are a combination of menu price increases and volume.

% Change in Foodservice and Drinking Establishment Sales (YoY % Change)

The most recent 3 months, compared to the prior year, also show strong growth.

We believe economic conditions for foodservice operators remain generally favorable as the consumer remains optimistic. Consumer sentiment over the past two years has remained at relatively elevated levels.

University of Michigan Consumer Sentiment Index

KA will continue to provide “Updates” on a periodic basis. We welcome your feedback on this issue and would appreciate hearing what other topics you would like us to cover in the future. And as always, we would be happy to discuss the information included on this particular edition or any other items concerning your business.

Bill Beattie Matt Austin

Email: bbeattie@keiteradvisors.com Email: maustin@keiteradvisors.com

Phone: 804.565.6018 Phone: 804.433.4184

| About Keiter Advisors |

| Our Foodservice Group is the only financial advisory team dedicated to the foodservice distribution industry. Over the past 14 years we have developed an expertise in the broadline, produce and protein segments. Our group has:

— Successfully closed 38 transactions |