By Scott Zickefoose, CPA, CM&AA, Transaction Advisory and Tax Senior Manager

Leveraging the Cash Conversion Cycle to Budget and Prepare your Business for the Future

Understanding your business’s cash conversion cycle is an important first step in budgeting and preparing for the future. This is true whether your business is in growth mode or capital preservation mode, as cash is often the largest constraint in both scenarios.

Your business’s cash conversion cycle is something that can appear simple at first, but more nuanced the more it is analyzed. This article serves as a primer on the cash conversion cycle and is not intended to cover the specifics and nuances of each phase of the cycle and each type of business. Each business will have a unique conversion cycle, which is impacted by factors such as contractual relationships, sourcing arrangements, vendor payment terms, etc.

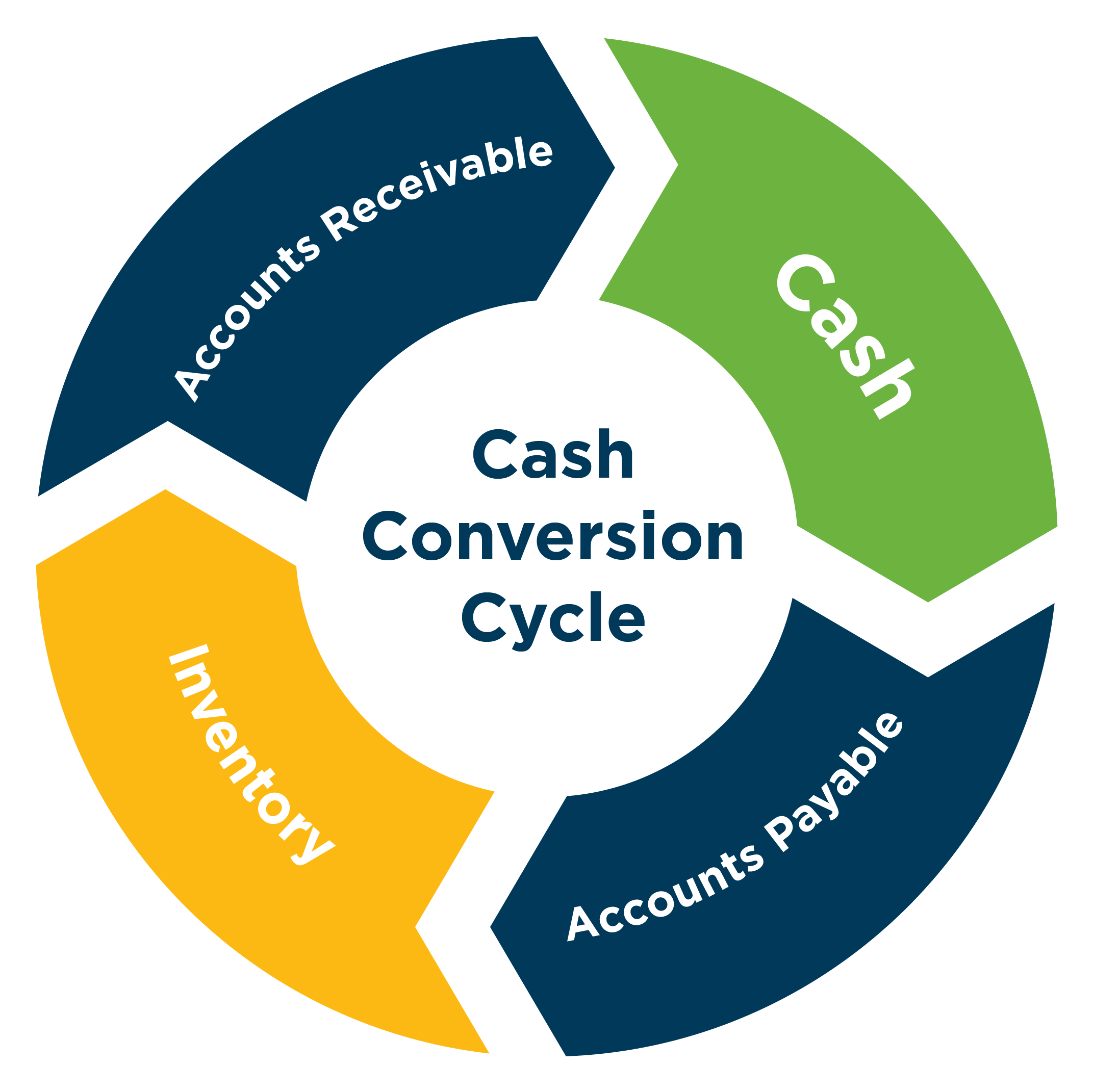

The cash conversion cycle measures how quickly a business can convert an investment, in inventory or otherwise, into cash from sales. Generally speaking, it is desirable for this cycle to be as short as possible, as this allows the most flexibility in management decision making and requires the least about amount of net working capital.

The cash conversion cycle is measured by the following formula:

Days Sales Outstanding (“DSO”) + Days of Inventory (“DIO”) – Days Payables Outstanding (“DPO”)

- DSO: [(Beginning AR + Ending AR)/2] / (Credit sales / 365)

- DIO: [(Beginning Inventory + Ending Inventory)/2] / (COGS / 365)

- DPO: [(Beginning AP + Ending AP)/2] / (COGS/365)

Management decisions to influence the cash conversion cycle have risks that should be considered. Keiter Advisors has prepared more in depth articles evaluating ways management can approach changing the cash conversion cycle as it relates to Accounts Receivable, Inventory, and Accounts Payable.

The Keiter Advisors team has significant experience assisting companies understand the drivers of their cash conversion cycle and thinking through ways of strengthening the cycle, in a variety of circumstances. If you are considering preparing a 13-week cash flow statement and would like assistance, please reach out to any member of the Keiter Advisors team.

Matt Austin Scott Zickefoose

Email: maustin@keiteradvisors.com Email: szickefoose@keitercpa.com

Phone: 804.433.4184 Phone: 804.273-6253